The Hidden Cost of Homeownership: Why Taxes Matter More Than Ever

When most people begin the homebuying process, their attention naturally gravitates toward the headline numbers—the purchase price, the interest rate, and the projected monthly payment. These are the figures that shape first impressions and often determine whether a property feels attainable. But there is another number, less visible at first glance, that ultimately defines the long-term reality of homeownership: taxes.

The Northeast

In today’s Northeast housing market, taxes are no longer a secondary consideration. They are a central force shaping affordability, influencing migration patterns, and redefining how buyers, sellers, and professionals’ approach real estate decisions.

The Northeast Reality: A Ranking That Speaks Volumes

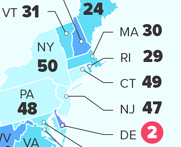

A closer look at four key states reveals just how significant the tax burden has become.

New York stands at the top of the list. For many homeowners, particularly in areas like Long Island and Westchester County, property taxes represent a substantial and ongoing financial commitment. These taxes are largely driven by school funding and layered local budgets, creating a structure where the annual tax bill can feel like an extension of the mortgage itself. As a result, buyers are increasingly asking not just whether they can afford the home today, but whether they can sustain the cost over time.

Connecticut follows closely behind, often without the same level of attention. At first glance, Connecticut may appear to offer value compared to New York, especially in terms of home prices. However, that perception can shift quickly once the tax structure is fully understood. High municipal mill rates and a strong reliance on property taxes for local services create a financial landscape that can narrow, or even eliminate, the perceived savings.

In Pennsylvania, the story is more nuanced. The state is frequently seen as a more affordable alternative, but its tax structure introduces complexity that can catch buyers off guard. Local earned income taxes, combined with school district-driven property taxes, vary widely depending on the municipality. This means that two homes with similar price points can carry very different long-term costs, making location a critical factor not just for lifestyle, but for financial planning.

New Jersey, while ranking fourth in this group, remains one of the highest-tax states in the nation overall. What distinguishes New Jersey is not the level of taxation, but the level of awareness surrounding it. Buyers entering the market are often more prepared for what they will encounter, and the tax burden is typically reflected more transparently in pricing and expectations. Even so, it remains a defining component of affordability across the state.

A Shift in How the Market Thinks

What is emerging across all four states is a fundamental shift in how real estate decisions are made. Affordability is no longer defined by the purchase price alone. Instead, it is shaped by a broader equation—one that includes taxes as a primary variable rather than an afterthought.

For buyers, this means taking a longer view. The initial excitement of securing a home must now be balanced with a clear understanding of the recurring costs that will follow year after year. For sellers, it introduces a new layer of strategy. Pricing a home effectively requires acknowledging not just its market value, but the total cost of ownership a buyer will inherit.

Real estate professionals, in turn, are finding that their role is evolving. The ability to guide clients through these conversations with clarity and confidence has become a defining advantage. It is no longer enough to know the market; one must understand the financial ecosystem surrounding it.

The Importance of Clarity in a Complex Environment

In a landscape where taxes play such a significant role, clarity becomes invaluable. This is where experienced title professionals make a meaningful difference. Obtaining accurate information, ensuring that municipal details are clearly understood, and helping all parties move forward with confidence are essential parts of the process. In an environment where uncertainty can carry real financial consequences, having a trusted partner brings stability to what can otherwise feel complex.

Redefining Affordability

There was a time when affordability could be measured by a single number. Today, it is better understood as a combination of factors working together—purchase price, financing, and, increasingly, tax burden.

Across New York, Connecticut, Pennsylvania, and New Jersey, taxes are often the element that makes the biggest difference over time. They influence not only what buyers can afford, but how long they can comfortably remain in the homes they choose. Understanding that reality is no longer optional.